Zero-based budgeting is income minus expenses will equal zero monthly. Tracking your expenses weekly or monthly are good options to keep a consistent personal budget.

Start by gathering all your credit card statements and bank accounts to track expenses. Review multiple statements, looking for your bills and when they are due. Understanding each statement and when you are expected to pay things will help you avoid fees.

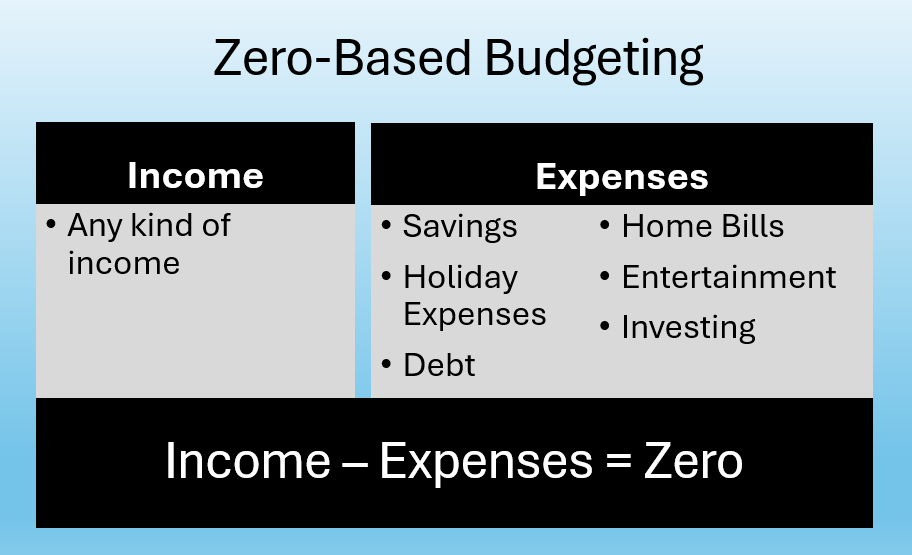

Income

This includes any type of income from tips, weekly checks and any side hustles.

Expenses

Savings

Planning for any saving goals from 5% or 20%. Understanding the amount of money put aside each month towards retirement, a home fund, emergency fund, or any other major purchases.

Home Bills

Any bill that is necessary for you to live, focusing on a roof over your head and food. Finding out the amount of income that goes to bills each month creates an easier job to track of the money spent. Categorize each bill into needs and wants to allow you to know what bills are flexible for your life and what’s not.

Holiday Expenses

Holidays, trips, and gifts can become expensive, so being prepared for it can help lower stress during those times. For example, setting a hundred dollars aside a month for gifts. While you are waiting for the time to spend this money put in investments or saving accounts, anything to gain interest, but do not let your extra money earn zero.

Entertainment

Find out the percentage of income that is spent on fun activities that includes any sports leagues, entertainment, going out to eat, ect…

Debt

Organize all of your debt and understand your goals, depending on the interest rates may change how each debt is paid off. There are mulitple methods such as snowball and avalanche method,

At the end of the month or week any extra money put towards your goals for retirement, savings, ect… Let the extra money you have work for you, do not let your money not gain interest. The point of the zero-based budget is to start each duration of your budget at zero.

Plan each category with income minues expenses equaling zero.